Examining the Effects of Dollarization on Ecuador

By Sam Wang, Research Associate at the Council on Hemispheric Affairs

To download a PDF version of this article, click here.

Every day since 2015, thousands of Ecuadorians have crossed the bridge from Tulcán, Ecuador to the border town of Ipiales, Colombia to go shopping. Goods they purchase in Colombia include food, cars, television, and even bulldogs. On a holiday weekend between May 27 and 29, more than 50,000 Ecuadorians crossed the border to Ipiales.[1] Some shoppers come from as far as Quito, a five-hour drive south of the border. Ecuadorians purchase goods in Colombia en masse due to a simple fact: prices in Colombia have become significantly cheaper. For example, a 50-inch TV costs $1,300 USD in Ecuador, but less than $800 USD in Colombia.[2] The situation has become of such concern to the Ecuadorian government that last year, President Rafael Correa issued a “call of conscience” to Ecuadorians, asking his compatriots to “offer support to the national production” by buying Ecuadorian products.[3]

In addition to Panama and El Salvador, Ecuador is one of the Latin American countries that uses the U.S. dollar as the only official currency. Ecuador does not print its own bank notes. In recent years, the U.S. dollar has continuously appreciated against other currencies in Latin America, making the price of goods in Ecuador higher than that in neighboring Colombia and Peru. Ecuador abandoned its old currency, the sucre, during a severe economic crisis in 2000 and has been using U.S. dollars ever since. With the appreciation of the U.S. dollar, doubts have emerged regarding the fate of dollarization. A recent Wall Street Journal article stated that Ecuador “has the misfortune to be an oil producer with a ‘dollarized’ economy that uses the U.S. currency as legal tender.”[4] The appreciation of the U.S. dollar against other currencies has decreased the net exports of non-oil commodities from Ecuador, which, coupled with the fall in oil prices, has constrained the country’s potential for economic growth.

The government of Ecuador has also cast doubt on the success of dollarization; as early as 2014, Correa said that “dollarization was a bad idea.”[5] In the same year, he established a parallel electronic currency for domestic use, which some believe is the first step of de-dollarizing the economy. However, proponents of dollarization believe that it has generated considerable macroeconomic benefits to Ecuador in the past 16 years. Through an examination of the impacts of dollarization in the 21st century and the economic principles behind it, this article argues that both the positive and negative impacts of dollarization are perhaps being overstated, and that a de-dollarization process would provide more negative effects than positive outcomes for Ecuador.

Why Dollarize?

Before delving into a discussion of the pros and cons of using dollars, one should first examine the history of dollarization in Ecuador. In the late 1990s, Ecuador experienced a severe economic crisis due to a combination of low oil prices, the low tax base of the non-oil sector, and big public sector wage increases.[6] The value of the sucre fell drastically, and the inflation rate galloped to 96.1 percent in 2000.[7] Ecuadorians first started adopting dollars informally in an effort to avoid losing their purchasing power, and massive capital flowed out of the country due to the exchange rate crisis.[8] In the same year, in order to halt capital outflow and hyperinflation, Ecuador decided to substitute its currency with the U.S. dollar. [9] The decision to dollarize the economy slowed hyperinflation, stopped the free fall of sucre, and stabilized the financial market, all of which significantly helped resolve the economic crisis. Although the exact impact of dollarization on Ecuador’s economic growth is beyond the scope of this study, after dollarization, Ecuador has enjoyed an average annual economic growth of 4.4 percent, higher than many Latin American countries.[10]

Benefits of Dollarization

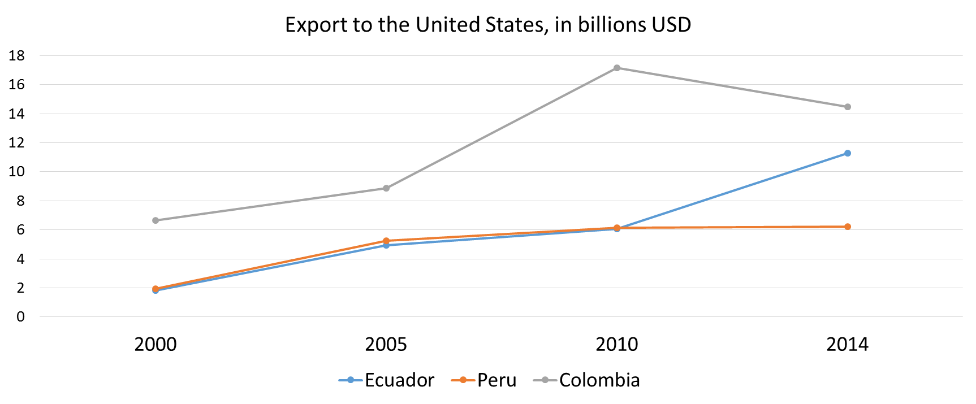

There are several benefits of dollarization that should be noted. Most evidently, it decreases transaction costs in international trade, which normally occur whenever people exchange one currency for another. Dollarization eliminates this cost in the trade with the United States, Ecuador’s largest trading partner, since businesses do not need to change from one currency to another. It also promotes long-term investment and trade since businesses tend to be reassured by the stability of the exchange rate.[11] In fact, Ecuador’s export to the United States has increased since dollarization, while the exports of neighboring Colombia and Peru, whose economies are both larger than Ecuador’s, have stagnated, although dollarization may not be the only factor of such an increase.

Source: Author’s elaboration with data from UN Comtrade

The second benefit of dollarization is a lower risk of inflation.[12] By using a foreign currency, an officially dollarized country assures itself of a rate of inflation close to that of the issuing country because confidence exists that inflation in the dollar will continue to be low.[13] However, it should be noted that the adjustment to lower rates took several years after the abandonment of the sucre. The inflation rate stayed at double digits in 2001 and 2002, and did not go below five percent until 2004.[14] Some economists predicted that inflation rates in Ecuador in the medium- and long-term would be relatively consistent with U.S. inflation rates, but in 2011 and 2012, it climbed up again to around five percent.[15] In comparison, the U.S. inflation rate since 2000 has never exceeded four percent.[16] Dollarization is not enough for a country to have a stable inflation rate. In the case of Ecuador, a developing country, the associated risk premium is still higher than that of the United States, a developed country with relatively high economic stability.

Proponents of dollarization also refer to another advantage: currency substitution prevents the Central Bank from having its own monetary policy. This seems very counterintuitive, since monetary policy is one of the two instruments that a government can use to influence a state’s economy. Proponents of dollarization argue that the elimination of a national currency means that government deficits must be financed through fiscal policies, which include the fairly transparent methods of raising taxes or accumulating debt, rather than through printing money.[17] Unlike the U.S. Federal Reserve, but similar to many central banks in Latin America, the Central Bank of Ecuador is not an independent institution but an agency of the executive branch. This is explicitly stated in Article 303 of the Constitution of Ecuador.[18] In the United States, the independent Fed is able to institute sound monetary policies that are not subject to the political whims of the administration, but when a central bank is in complete control of the executive branch, there is a possibility that the government would implement expansionary monetary policies intended to provide an economic stimulus before elections or finance a growing government budget deficit. In both situations, an overly aggressive expansionary monetary policy would lead to a rising inflation rate and a falling exchange rate, which would contribute to destabilizing the economy. Such cases have occurred in the past in Argentina and Venezuela.[19] Proponents of dollarization argue that it gets rid of the moral hazard, by which politicians can infinitely finance public spending by increasing the money supply, and instead leads to budgetary discipline and more responsible government spending.

Putting aside the questions regarding whether Latin American governments are capable of developing sensible monetary policies and whether an independent central bank is preferable, dollarization does not fully address its proponents’ concern of growing public spending, since it does not curb expansionary fiscal policies. The government expenditure of Ecuador has increased from 20 percent of the GDP in 2000 to a high 44 percent in 2014.[20] In comparison, the government expenditure of Colombia, Peru, and Mexico has never exceeded 30 percent of their respective GDPs since 2000.[21] Consequently, since the Ecuadorian government cannot print money, it financed spending through debt. In the past decade, the debt-to-GDP ratio has also increased from a low of 16.4 percent to 33.1 percent in 2015.[22] The increasing government debt has not reached an alarming level, but the considerable increase in government spending necessitates caution. The government of Ecuador has taken steps to address the issue; in April, President Correa announced a two percentage point increase in sales tax, a new wealth tax for millionaires, and the possible sale of government assets.[23] These measures will help finance an increasing budget and maintain fiscal sustainability. Nevertheless, dollarization does not impact fiscal policies, and has virtually no effect on the rising budget.

Disadvantages of Dollarization

The biggest advantage of dollarization in the eyes of its supporters is precisely the reason why others are critical of it—the central bank is unable to have its own monetary policy. The use of the U.S. dollar as legal tender means that one of the two instruments for influencing the economy is unavailable to the government. The absence of monetary policy, besides making it harder for the government to intervene during times of recession, has an adverse effect on exports. A weak domestic currency stimulates exports, and a strong domestic currency makes the country’s exports less competitive in the international market compared to goods from other countries.[24] In the past two years, the U.S. dollar has appreciated considerably; the dollar index, which measures the relative value of the U.S. dollar against a basket of foreign currencies, has risen about 25 percent since 2014.[25] This makes Ecuador’s exports less competitive in the international market. In fact, in 2015, Ecuador’s non-oil export value dropped by 5.9 percent from the previous year.[26] In comparison, products from countries such as Colombia and Peru, both of which saw their currency depreciate against the dollar, became relatively cheaper and more competitive.

Even during times when the dollar is not rising, the instrument of monetary policy would give Ecuador an option to stimulate the economy through “competitive devaluation,” which refers to the strategic and large-scale depreciation of a domestic currency to boost export volumes.[27] For example, starting in 2013, the Japanese government deliberately depreciated its currency in order to make Japanese exports more competitive.[28] Without the option of implementing such policy, Ecuador’s exporters are dependent on the fluctuations of the market. Especially in times of economic crisis, countries without monetary policy have to go through internal devaluation, which restores competitiveness by reducing labor costs. and is often a much longer and more painful process.

Despite the benefits of having control on monetary policy, a de-dollarization in Ecuador would not do much to help its export sector, given that the underlying problem is that Ecuador’s economy is dependent on oil. The dependence has been a structural problem ever since Ecuador discovered its oil resources. In 2014, 52 percent of Ecuador’s export value came from petroleum.[29] Since then, oil prices have fallen significantly; the Brent Crude decreased from $100 USD per barrel to less than $50 USD today, which dealt a heavy blow to the economy of Ecuador.[30] The dominance of the oil sector makes it extremely hard to rely upon monetary policies to boost export for two reasons. First, a currency depreciation does not help oil export because oil is priced and traded in a world price denominated in U.S. dollars. A country’s capacity to produce oil is also limited; Ecuador cannot immediately increase oil production even if there is a sudden increase in demand. Second, the revenue brought in by oil exports is in U.S. dollars. If Ecuador de-dollarizes, a large and constant inflow of U.S. dollars would lead the national currency to appreciate because there will be a constant demand for changing the petrodollars to the national currency, whereas export sectors, such as manufacturing gain an advantage when the national currency depreciates. This means that the positive, effect of a currency depreciation on exports would be largely offset by the effect of petrodollars. In order to overcome the petrodollar effect, oil-producing countries have to depreciate their currencies much more than non-oil-producing countries to increase export value. However, a country cannot permanently conduct expansionary monetary policies, since doing so would both lead to a high inflation rate and encourage irresponsible government spending.

Moreover, placing the responsibility of boosting exports solely on currency depreciation would potentially neglect other ways to promote exports. In 2011, Colombia and Peru, Ecuador’s only neighbors, joined the Pacific Alliance with Mexico and Chile. The regional trade block has eliminated tariffs on over 92 percent of goods, eased intra-Alliance visa restrictions, and integrated stock markets of their members.[31] The elimination of tariffs makes goods from those four countries more competitive in other countries of the Alliance. Especially relevant is the advantage afforded to Colombia, whose banana and flower industries are as significant and competitive as Ecuador’s. Ecuadorian exporters will face increasing competition with their Colombian counterparts when they sell goods to Mexico, Peru, and Chile. Instead of fixating on the issue of dollarization, the government of Ecuador and international economists should be more inclined to promote regional economic integration and abolish tariffs between Ecuador and other Latin American countries.

Concluding Remarks

Both supporters and opponents of dollarization have overstated the policy’s effects on the Ecuadorian economy. Dollarization is not a sole remedy for all economic problems, but neither is having a national currency. De-dollarizing the economy today would trigger market uncertainty and lead to economic instability, which would inevitably hurt Ecuador. Furthermore, the fact that Ecuador’s economy is heavily dependent on oil is a sad but unavoidable truth that cannot be changed in the short term. This is not to say that the government should significantly shrink the oil sector—oil revenue is a crucial source of funding for social projects that benefit the lower class. Nevertheless, to offset the negative effects of using U.S. dollars, Ecuador should enact policies that maintain macroeconomic stability, such as setting up a rainy day fund for economic downturns, and promote regional trade and integration to boost its exports within the region.

By Sam Wang, Research Associate at the Council on Hemispheric Affairs

Original Research on Latin America by COHA. Please accept this article as a free contribution from COHA, but if re-posting, please afford authorial and institutional attribution. Exclusive rights can be negotiated. For additional news and analysis on Latin America, please go to: LatinNews.com and Rights Action.

Featured Photo: U.S. Dollars. Taken from Google Images.

[1] “Ipiales, La Despensa Colombiana De Ecuador.” EL PAÍS. 2016. Accessed July 13, 2016. http://internacional.elpais.com/internacional/2016/06/20/america/1466376543_846138.html.

[2] “¿Por Qué Correa No Quiere Que Ecuatorianos Compren En Colombia? – Latinoamérica – El Tiempo.” El Tiempo. Accessed July 13, 2016. http://www.eltiempo.com/mundo/latinoamerica/por-que-correa-no-quiere-que-ecuatorianos-compren-en-colombia/16343555.

[3] “Ecuador Les Pide a Sus Ciudadanos No Comprar En Colombia.” CNNEspañol.com. 2015. Accessed July 13, 2016. http://cnnespanol.cnn.com/2015/09/02/ecuador-le-pide-a-sus-ciudadanos-no-comprar-en-colombia/.

[4] Cui, Carolyn. “Cheap Oil and Strong Dollar: Ecuador’s Twin Troubles.” WSJ. Accessed July 13, 2016. http://www.wsj.com/articles/cheap-oil-and-strong-dollar-ecuadors-twin-troubles-1448320496.

[5] “Correa Says ‘dollarization Was a Bad Idea’; Says That Ecuador’s Reliance on the Dollar Puts Country in a Financial ‘straight Jacket’ | CuencaHighLife.” CuencaHighLife. 2014. Accessed July 13, 2016. http://www.cuencahighlife.com/correa-says-again-that-dollarization-was-a-bad-idea-says-that-ecuadors-reliance-on-the-dollar-puts-country-in-a-financial-straight-jacket/.

[6] “Ecuador and the IMF.” IMF. Accessed July 13, 2016. https://www.imf.org/external/np/speeches/2000/051900.htm.

[7] “Ecuador Inflation Rate (consumer Prices).” Index Mundi. Accessed July 13, 2016. http://www.indexmundi.com/ecuador/inflation_rate_(consumer_prices).html.

[8] “Ideas Have Consequences: The Case of Dollarization in Ecuador.” Atlas Network. Accessed July 14, 2016. https://www.atlasnetwork.org/news/article/ideas-have-consequences-the-case-of-dollarization-in-ecuador.

[9] Ibid.

[10] “Dollarisation in Ecuador.” Adam Smith Institute. Accessed July 13, 2016. http://www.adamsmith.org/blog/international/dollarisation-in-ecuador.

[11] “Basics of Dollarization.” Global Policy Forum. Accessed July 13, 2016. https://www.globalpolicy.org/pmscs/30435.html.

[12] “Dollarization Explained | Investopedia.” Investopedia. 2004. Accessed July 15, 2016. http://www.investopedia.com/articles/04/082504.asp.

[13] Ibid.

[14] “Official Dollarization and the Banking System in Ecuador and El Salvador.” Federal Reserve Bank of Atlanta. Accessed July 13, 2016.

[15] “Ecuador Inflation Rate | 1970-2016 | Data | Chart | Calendar | Forecast.” Trading Economics. Accessed July 13, 2016. http://www.tradingeconomics.com/ecuador/inflation-cpi.

[16] “United States Inflation Rate (consumer Prices).” Index Mundi. Accessed July 15, 2016. http://www.indexmundi.com/united_states/inflation_rate_(consumer_prices).htm

[17] “Basics of Dollarization.” Global Policy Forum. Accessed July 13, 2016. https://www.globalpolicy.org/pmscs/30435.html.

[18] “República Del Ecuador Republic of Ecuador Constitution of 2008 Constitucion De 2008.” Ecuador: 2008 Constitution in English. Accessed July 13, 2016. http://pdba.georgetown.edu/Constitutions/Ecuador/english08.html.

[19] “10000 Years of Economy.” Cité De L’Économie Et De La Monnaie. Accessed July 13, 2016. http://www.citeco.fr/10000-years-history-economics/contemporary-world/hyperinflation-in-argentina.

[20] “Ecuador – Gasto Público 2016.” Datosmacro.com. Accessed July 13, 2016. http://www.datosmacro.com/estado/gasto/ecuador.

[21] Ibid.

[22] “Ecuador Government Debt to GDP | 1990-2016 | Data | Chart | Calendar.” Trading Economics. Accessed July 13, 2016. http://www.tradingeconomics.com/ecuador/government-debt-to-gdp.

[23] Casey, Nicholas. “Earthquake Jolts Ecuador Into Enacting Long-Avoided Fiscal Changes.” The New York Times. 2016. Accessed July 13, 2016. http://www.nytimes.com/2016/04/24/world/americas/earthquake-jolts-ecuador-into-enacting-long-avoided-fiscal-changes.html?_r=1.

[24] “Interesting Facts About Imports And Exports | Investopedia.” Investopedia. 2013. Accessed July 13, 2016. http://www.investopedia.com/articles/investing/100813/interesting-facts-about-imports-and-exports.asp.

[25] “U.S. Dollar Index (DXY).” Market Watch. Accessed July 13, 2016. http://www.marketwatch.com/investing/index/dxy.

[26] “Download Trade Data.” UN Comtrade. Accessed July 13, 2016. http://comtrade.un.org/data/.

[27] “Interesting Facts About Imports And Exports | Investopedia.” Investopedia. 2013. Accessed July 13, 2016. http://www.investopedia.com/articles/investing/100813/interesting-facts-about-imports-and-exports.asp.

[28] “Japan’s Devaluation Warning for Europe.” WSJ. Accessed July 13, 2016. http://www.wsj.com/articles/japans-devaluation-warning-for-europe-1426548519.

[29] “What Did Ecuador Export in 2014? @Atlas_facts.” What Did Ecuador Export in 2014? Accessed July 13, 2016. http://atlas.cid.harvard.edu/explore/tree_map/export/ecu/all/show/2014/.

[30] “Brent Crude (Sep’16) (@LCO.1 :).” CNBC. Accessed July 13, 2016. http://data.cnbc.com/quotes/@LCO.1.

[31] “B|Brief: The Pacific Alliance 2.0 – Next Level Integration.” Bertelsmann Foundation. Accessed July 13, 2016. http://www.bfna.org/publication/bbrief-the-pacific-alliance-2-0-next-level-integration.