Canada’s Financial Dominance in the Former English Caribbean Colonies (FECC)

By Tamanisha Jennifer John, Extramural Contributor at the Council on Hemispheric Affairs

To download a PDF of this article, click here.

Introduction

Today, Canadian Banks dominate the financial industry of the Former English Caribbean Colonies (FECC), enhancing and often enriching the external interests of capital for their banks in Canada. This is done at the expense of internal solutions to development of these Caribbean states. The story of Canadian corporate ownership of financial institutions in the region is not new. IMF Structural Adjustment Programs (SAPs) in the 1980s-1990’s solidified the region’s banking sector in the hands of Canadian corporations. Canadian monopolistic ownership of Caribbean finance has a very rich history that speaks to what Canadian banking concentration in the region looks like— not just during centuries of colonial exploitation— but also of neoliberal exploitation in today’s free-market era. The political economy of FECC is one structured by debt being serviced through a narrow Canadian ownership structure that frequently contradicts FECC sovereignty and economic security.

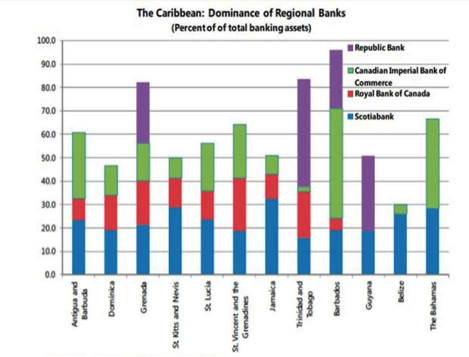

Of the five largest banks in Canada, three of them—Royal Bank of Canada (RBC), Bank of Nova Scotia (Scotiabank), and Canadian Imperial Bank of Commerce (CIBC FirstCaribbean)—operate in the FECC as dominant financial institutions acting as subsidiaries (Figure 1)[1]. The subsidiary status of Canadian banks in FECC is of paramount importance because, unlike a foreign branch bank, a subsidiary is not required to give out loans to Caribbean companies. However, what they are allowed to do is raise capital and issue debts and loans to corporations and governments. Canadian banking presence in FECC started due to traditional colonial ties with Britain which facilitated their operation in the region beginning in the late 19th to the early 20th century. This presence was fueled by colonial trade between the Maritime provinces of Canada and the West Indies under British rule in 1882.[2] Trade and access to commerce with American finance was a motivating factor for Canadian banks’ expansion in the region. RBC and Scotiabank, were the first Canadian banks to commence operating in the FECC. Thus, although expansion of Canadian banks in the region has a long history, there will be a particular focus in the time period when it peaked during the financial crises of the 1980’s— which prompted specific (external) policy recommendations that aided in further concentration of Canadian banks in the region today.

It should be noted that due to the colonial history of Canadian banking in the region, one could make the argument that Canadian banks have always been concentrated in FECC, even before these states became fully independent. After all, by the mid-1970’s “Canadian banks controlled 60-90 per cent of banking in the Commonwealth Caribbean”.[3] This information is important for understanding the increased prominence of Canadian banks in the region during the 1980’s, because towards the latter half of the 1970’s, Canadian banking influence in the region started to wane as a result of criticism from Caribbean nationals. Questions of how the region could be free from Western domination if their economic potential was dependent upon, and controlled by, foreigners became popular. This connection between Western domination and Canadian banking became apparent because Canadian takeover of financial institutions positively correlated with increasingly limited access to capital by Caribbean nationals and small firms for development usage, as well as increasing foreign control of profitable sectors.[4]

As a result, during the 1970s “Canadian banks, in Trinidad [and Tobago], were targeted in demonstrations and even fire bombings” in an effort to encourage them to leave the country as well as the region.[5] During this period of regional turmoil, a Canadian External Affairs Official, when asked to address the protests against Canadian financial institutions throughout the region, was quoted as saying “we’re not colonialists by intent, but by circumstances. We’ve taken on a neocolonial aura there [in the Caribbean].”[6]

Therefore, when I state that Canadian financial institutions were enabled during the 1980’s and 1990’s by IMF SAPs to regain their pre-1970’s colonial status within the region, it should not be taken lightly. The resurgence of these Canadian financial institutions after the implementation of IMF SAPs by FECC states allowed them to become deeply embedded within the financial architecture of FECC. The results of this embeddedness have been the increasing reliance on private sector credit and continued Canadian concentration within the region. It would be difficult to discuss access to private sector credit and the increasing reliance on private sector credit by FECC states separate from the concentration of Canadian financial institutions. This is because the inability of small private firms to gain access to credit or loans is related to whether these Canadian financial institutions see these firms as being worthy, that is, profitable enough to receive credit. And secondly, the benefits Canadian financial institutions seek to gain from providing credit or loans to FECC states themselves is related to their concentration within FECC states. Concentration of Canadian financial institutions and the switch to relying on private sector credit comes out of a colonial and neocolonial history in FECC, which explains the present-day build-up of debt via private creditors and Canadian concentration.

Canada’s Entrance into FECC

In discussing the financial stranglehold of Canadian banks and other foreign financial institutions in his home country of Trinidad during the 1970’s, Afro-Trinidadian historian and journalist C.L.R. James described conditions in Trinidad:

You get off at Piarco [airport] and you take a taxi to the chief town which is Port-of-Spain. You turn up the main street and within 200 yards, you stop. Independence Square. Good! so you pull up the taxi and you say. Well, this is a fine square. You have some magnificent buildings here. Yes. You ask him, what is that building? He says, that is Barclay’s Bank. And what is that building? That is the Canadian Bank of Commerce. And what is that big one next to it? That’s the Royal Bank of Canada. And what is that big one over there? That is Chase Manhattan. And what is that one? That is the Bank of London and Montreal. And that one? That is the Bank of London and Halifax. In other words, Independence Square is surrounded by some of the most magnificent buildings in the territory and all of them are foreign banks. That’s how we live. They rule the place.[7]

According to Peter Hudson,[8] James was right. During his description of Trinidad, Hudson pointed out “Canadian banks controlled 60 per cent of Trinidad’s commercial and retail banking. For the rest of the Commonwealth Caribbean [aka FECC], the figure ranged between 60 and 90 per cent.”[9] This type of concentrated foreign ownership of a sovereign entity’s financial system is unprecedented—especially when one considers that it is a colonial holdover which became codified in the region before, during, and after fights for independence. Although governments within the region— and other smaller indigenous banks— did try to compete with the Canadian banks, they simply could not.

Under colonialism and during the British Empire, Canadian banks provided the financial muscle and “colonial monetary functions that would uphold an [intra] imperial financial and commercial architecture.”[10] What this means is that Canadian financial ownership became so institutionalized within the region because it was beneficial to imperial forms of trade (British → Canada; American → Canada).[11] This institutionalization was pushed by Canadian bankers, in light of their failed attempts at annexing the British West Indies from the British.[12] Thus, “substituting political ties for economic tethers” Canadian financial institutions “embarked on a major push in the Anglophone Caribbean through a strategy that combined mergers and acquisitions of existing institutions”[13]— as British selling of its colonial territories to Canada never was an option.

To outcompete the British within their own territories, Canadian financial institutions diversified their range of operations—even acting as “government depositories and in some cases floating sovereign debts.” Therefore, these institutions successfully became the preferred institutions of British subjects—including the wealthy Caribbean elites and the peasant African and Indian workers—including the illiterate, who could now open saving accounts with less than a dollar.[14] These Canadian banks also opened remittance accounts for Caribbean workers abroad who were working in the coal mines of Canada.[15] As proof of their institutionalization in FECC, even over the Crown, Hudson writes that “the most telling sign of the Royal Bank’s strength in the Caribbean comes not from the counting of branch banks, the increase in deposits, or the aggregate figures of loans but through popular culture. Every year, the Royal Bank Magazine, [wrote] a calypso for carnival whose subject was the [Canadian] Bank.”[16]

In this context, the switch to independence (and pre-expansionary Wall Street), resulted in continued Canadian ownership. Hudson writes that “in the absence of a developed American banking presence, [Canadians] lent [their] financial machinery to American corporations facilitating U.S. trade and commercial operations in the Caribbean and, occasionally, providing the financial machinery for U.S. colonial governance.”[17] Protests against Canadian financial institutions during the late 1960’s and especially during the 1970’s erupted due to increasingly limited access to capital by Caribbean nationals and small firms, and the increased Canadian control of profitable sectors which were seen as being colonial in nature. Due to the successful institutionalization and accessibility (high number) of these Canadian banks, national government savings banks and indigenous credit associations found themselves unable to compete[18] with an already embedded financial architecture ruled by Canadian banks. The turmoil against these enterprises attempted to undermine public confidence in the banks, and by implication attack racism and neocolonialism.[19]

IMFs Facilitation of Canadian Financial Institutions Dominance in FECC (1980s SAPs)

Thus, Canadian ownership of financial institutions within the region had to face rising Caribbean consciousness of exploitation by these institutions. The resurgence of these Canadian financial institutions in the 1980’s-1990’s—understood to be exploitative within the region—could only happen in light of IMF-mandated reforms. Unfortunately, the unique positioning of these banks after the implementation of IMF SAPs was due to the failure of the 1970’s FECC turmoil against Canadian financial institutions to address the economic structures (institutionalization) that facilitated these Canadian banks’ presence since the colonial period. What this means is that during the turmoil of the 1970s, Caribbean governments, elites, and nationals focused on decolonization and the “racial holdovers of colonialism, [which] did not represent anything near to a radical critique of the racial and economic structures facilitating Royal Bank’s practices of accumulation. Nor did this moderate critique propose structural reforms within the political economy of decolonization in an era of neocolonialism.”[20]

In the 1960s and 1970s protestors in the FECC demanded that Canadian banks institute localization policies. However, these policies had “little effect on power relations” and usually resulted in these banks repatriating all of their profits before including a local figurehead.[21] After these local figureheads were installed many of these institutions simply dropped ‘Canada’ from their name and added a regional moniker (e.g. Canadian Imperial Bank of Commerce (CIBC) → First Caribbean International Bank).[22] The reforms implemented by the IMF were influenced by neoliberal policies based on austerity, the benefits of the free market, free trade as a trade doctrine, deregulation, decreased government spending, increased role of the private sector, and more. Unsurprisingly, this had the effect of creating a favourable environment for foreign entities and investors, at the expense of these countries that were unable, due to crises, to compete in the free market, because they specialized in cheap commodity goods. The only institutions in a position to benefit from such reforms, were these foreign colonial Canadian institutions that were not quite out of the region following the 1970’s turmoil. These Canadian institutions had the means, capital, and access to networks of (Canadian) investment, that Caribbean states tended to lack.

During the economic crises which shook the Third World in the 1980’s, Canadian financial institutions embarked on an almost-total pull out from the FECC, selling most of their interests to local capitalists and regional governments with prices ranging between 1 dollar and 6 million dollars.[23] What is telling about the selling of their interests, is that these Canadian corporations’ buy-backs in the region coincided with the exact same time that FECC governments implemented IMF SAPs. In 1984, Canada’s RBC bank “sold its assets in Guyana to the Guyanese government for 1 dollar (a transaction repeated by both National City Bank and Barclays).”[24] During that same year, Guyana’s government borrowed money from the IMF, and one year later in 1985 Guyana was ineligible to receive further funds without the implementation of an IMF SAP due to deteriorating recovery from the crisis.[25] In 1989, the government of Guyana was listed as the poorest country in the Western Hemisphere—and this became the first time a country beat out Haiti for that position.[26] Thus, Guyana underwent an intensive IMF SAP chaired by a Canadian support group[27] to turn the Guyanese economy around by facilitating the raising of funds for the Guyanese government through Canadian (and American) buyback of assets and public utilities.[28]

During this time, bauxite miners, sugarcane cutters, students and teachers in Guyana— who could no longer afford the bus fare— started to picket the Canadian High Commissioner’s Office demanding an end to the strict austerity program because of the SAP that the Commissioner had recommended to the IMF for Guyana.[29] The Canadian support groups to the IMF recommended that Guyana institute an intensive austerity plan that required a 230 per cent currency devaluation, a 35 per cent rise in interest rates, and a 20 per cent wage increase.[30] It should also be noted that the 20 per cent wage increase only occurred in order for Guyanese to be able to afford a loaf of bread, one-half a pound of chicken, OR (not and), a gallon of rice.[31] Although the Canadian High Commissioner, Frank Jackman at the time, noted that these budgetary measures were unpopular, he expressed satisfaction on a local broadcast that the Guyanese people should be reassured that “the austerity package would encourage Canadian multinational corporations to look favourably on Guyana in making decisions about where to invest.”[32] Canadian purchases and investments would thus enable the Guyanese government to meet its debt payments on schedule, because Canadian support groups reasoned that money saved—through reducing social and welfare projects along with selling of assets—would be able to pay Guyana’s debts back to the IMF.

The IMF pursued a similar corporate development strategy throughout the FECC states,[33] which were encouraged by the Canadian banking community and various Canadian support groups set up specifically for the region.[34] The corporate development strategy via IMF SAPs allowed foreign buyers, including American and European buyers, to buy financial banking assets within the Caribbean. Canadian banks sold their interests in Trinidad and Tobago in 1987 to the Royal Bank of Trinidad and Tobago (RBTT),[35] and in 1989 Trinidad and Tobago implemented IMF SAPs and Canadian buy-back started to help them service IMF debts. It should be noted here that American and European buyers also entered the picture as foreign entities able to profit from the region in light of IMF SAPs.[36] In 1987 Canadian banks sold their 48 per cent stake in Jamaica’s Royal Bank to Jamaica Mutual Life Assurance,[37] and in 1989, with the implementation of IMF SAPs, foreign entities started buying stakes in Jamaica.[38]

The same thing occurred in Belize in 1987 when Canadian banks were sold to Belizean investors.[39] Belize then underwent an IMF SAP and the foreign buy-back started. As such, the crisis did not mark the end of Canadian banks in the FECC, but rather just a brief hiatus. After this, Canadian banks made their biggest push back into the region since their colonial introduction, facilitated by IMF reforms. Unsurprisingly, in 1989 during Canadian financial re-entry into FECC, Allan Taylor, the chairman of the Royal Bank, convinced Canadian support groups and the IMF (with the approval of the Canadian banking community) that “foreign investment in the borrowing countries would have to play a much larger role in resolving [their] debt[s].”[40] Which of course, would benefit the stockholders of the foreign banks that are making the “investment.”

Additionally, borrowing from Canadian subsidiary banks as a means to address development problems became plausible because of the new perception put forward by these banks during their resurgence in the 1980’s. During the days of independence for FECC, one of the major effects and criticisms of Canadian financial institutions in the region was “the diversion of funds from local industry to the bank’s country of origin.”[41] During the 1980’s when IMF SAPs were starting to be implemented, Canadian financial institutions came back with two new strategies to stave off scrutiny which began to function in the 1970’s. First, they sought to promote Canadian investment through acquisitions which would help them to retain local market shares in the region.[42] And second, there was intensification of Canadian aid programs to the region, which were praised by the IMF.[43] Interestingly enough, former Canadian representatives to the IMF were the ones heading these aid programs.[44] This is important, as it was these very same Canadian aid programs which facilitated the raising of funds by FECC states through advising FECC governments to sell private industry to foreign, mostly Canadian and U.S., buyers.[45]

Continuing Access to FECC for Canadian Financial Institutions

Of course, IMF reforms during the 1980’s did not automatically grant Canadian corporations the return to their colonial status. As previously mentioned, during the 1980’s, implementation of IMF SAPs also allowed American and European investors to purchase assets in FECC. These interests being purchased by foreigners from FECC governments and national capitalists included former Canadian interests which were sold during FECC states’ crises. From the 1990’s Canadian financial institutions’ preferred method of interaction with FECC governments was through the use of trade agreements and aid after the implementation of IMF SAPs.[46] In the year 1990, Canadian Prime Minister Brian Mulroney announced plans to increase aid to the Caribbean region, enhance access to Caribbean rum in Canada, and to forgive the debt of 11 Caribbean countries—of which 8 belonged to FECC— of up to 182 million dollars.[47] This amount of debt forgiveness was the last major initiative undertaken by Canada within the region.[48]

In 1993, the Canadian Regional Development Program was initiated in the Caribbean to regularly provide between 30 – 35 million dollars per year to fund infrastructure projects.[49] The program evolved throughout the early 90’s to include investments in human resource development, private sector development, trade policy development, and public sector economic management.[50] This effectively led to what Paget Henry called the “transformation of Caribbean labour itself into a commodity framework,”[51] as it allowed for the increased migration of Caribbean labour abroad to Canada in mining and farming from mostly FECC countries.[52] This also contributed to the continuous brain-drain from FECC countries during the mid-1990’s and early 2000’s.[53] According to Mary Anne Chambers, Senior Vice President of Scotia Bank (1998-2002): “I served on the Board of two Ontario hospitals, where the Chiefs of Surgery, Pediatrics, and Psychiatry were all University of the West Indies medical graduates.”[54]

In 1998, the increasing benefits of Canadian aid and lenient workers’ programs towards the region started to come under question. The uniqueness of the deal was first recognized by Canadian rum exporters who had hoped to benefit from Canada’s 1998 protocol on rum. In 1998, the CARIBCAN agreement went into effect, which granted unilateral duty-free access to eligible goods from FECC (up until 2011).[55] After the agreement was implemented, however, FECC rum still faced formidable barriers gaining access to Canadian markets. Unequal trade deals thus marked the relationship between the FECC and Canada throughout the late 1990’s up until 2006. Ramesh Chaitoo notes that in spite of the Caribbean being unable to take real advantage of any market access granted by Canada, Caribbean states continued to enter agreements with Canada. This is because Canada was generous throughout this period in granting aid to the region, in comparison to other donors.[56] Thus, this time period marked further dependence by FECC on Canada. In 2002, Canada granted duty free access to the world’s 48 least developed countries. In the Caribbean region, Haiti was the only country that qualified.[57] Additionally, during this time period (2002-2006), Canadian foreign direct investment (FDI) in FECC increased annually in the financial services sector.[58] In 2007, as part of a trade deal between Canada and the FECC, Canada increased aid to the region to 600 million dollars.[59] Although many within FECC thought the amount was too small, as the deal would grant Canada even more market access within the region, it still passed. The general trend throughout the decade of the 2000’s was growing Canadian access to Caribbean markets, as Canada threw aid at the region in order to pass trade agreements which provided little benefit to the region.

In 1998, the increasing benefits of Canadian aid and lenient workers’ programs towards the region started to come under question. The uniqueness of the deal was first recognized by Canadian rum exporters who had hoped to benefit from Canada’s 1998 protocol on rum. In 1998, the CARIBCAN agreement went into effect, which granted unilateral duty-free access to eligible goods from FECC (up until 2011).[55] After the agreement was implemented, however, FECC rum still faced formidable barriers gaining access to Canadian markets. Unequal trade deals thus marked the relationship between the FECC and Canada throughout the late 1990’s up until 2006. Ramesh Chaitoo notes that in spite of the Caribbean being unable to take real advantage of any market access granted by Canada, Caribbean states continued to enter agreements with Canada. This is because Canada was generous throughout this period in granting aid to the region, in comparison to other donors.[56] Thus, this time period marked further dependence by FECC on Canada. In 2002, Canada granted duty free access to the world’s 48 least developed countries. In the Caribbean region, Haiti was the only country that qualified.[57] Additionally, during this time period (2002-2006), Canadian foreign direct investment (FDI) in FECC increased annually in the financial services sector.[58] In 2007, as part of a trade deal between Canada and the FECC, Canada increased aid to the region to 600 million dollars.[59] Although many within FECC thought the amount was too small, as the deal would grant Canada even more market access within the region, it still passed. The general trend throughout the decade of the 2000’s was growing Canadian access to Caribbean markets, as Canada threw aid at the region in order to pass trade agreements which provided little benefit to the region.

During the 2008 financial crisis, many pundits were certain that the Caribbean region would be fine despite the major sources of their tourist arrivals being from the U.S. and E.U.—because there were no subsidiaries of foreign banks from the U.S. or E.U. within the region.[60] Almost all the banks operating in the region were wholly or partially owned by firms headquartered in Canada—which was the developed country least impacted by the crisis. Additionally, the Canadian banks that were operating in the region acted as subsidiaries rather than branches, which would further protect these Caribbean states. However, this turned out not to be the case. Of the broad category—Latin America & the Caribbean— the Caribbean was hit hard in its productive and financial sectors.[61] In any event, like the crises in the 1980’s and 1990’s which allowed increased Canadian investment and corporations to enter the region at alarmingly high rates, due to IMF incentives for foreign investors, the aftermath of the 2008 crisis solidified the Canadian corporations’ monopoly on Caribbean financial institutions.[62]

The increased acquisitions and mergers by Canadian financial institutions which took place in FECC during the 2007/2008 financial crisis—during which many American and European investors sold their interests to Canadian and Japanese banks—allowed Canadian financial corporations to regain their colonial status in terms of financial ownership.[63] Needless to say, as in the aftermath of the 1980s crises, Canadian institutions became major creditors for FECC during the ‘08 crisis through Canadian-formed support programs which facilitated their corporate buy-backs and acquisitions of other foreign entities’ interests.

The whole notion of Canadian institutions lending money to FECC states as private creditors seems almost ludicrous, as FECC still had high amounts of debt owed to the IMF both before and after the crises. However, banks were incentivized after the financial crisis of 2008 to issue debt “because it [became] cheaper than [holding] equity.”[64] Additionally, most FECC states “retain[ed from colonialism] punitive system[s] of bankruptcy law, based on the old English model of bankruptcy practice,” meaning that many FECC states had “creditor friendly” laws which helped them gain access to private credit at the debtor’s expense.[65] Thus, domestic debt was allowed to assume a larger role in FECC only after these countries experienced greater difficulty in accessing international loans.[66] The turn to domestic debt only further exposed the institutional weakness of FECC, in the form of punitive domestic credit laws, stemming from the colonial period.

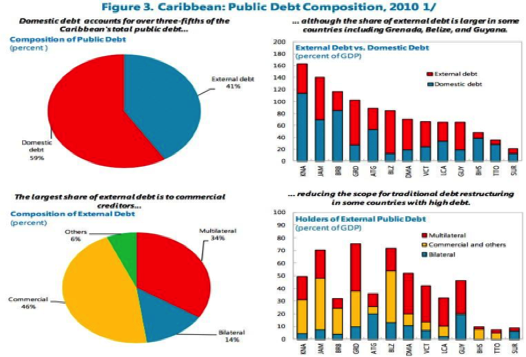

Due to the subsidiary status of Canadian financial institutions, between 2012 and 2013 FECC domestic debt accounted for a little under three-fifths of FECCs total public debt, or 59 per cent—meanwhile external debts accounted for 41 per cent.[67] External debts include debts owed to multilateral institutions (largely the IMF & WB at 34 per cent), bilateral agreements (state to state at 14 per cent), and others (at 6 per cent).[68] Domestic debts are debts owed to national financial institutions, including commercial banks (36 per cent), non-bank financial institutions (27 per cent), and social security schemes (20 per cent).[69] Figure 3 by the IMF details the decreasing reliance on public (meaning external) debt in 2010.[70]

Figure 4

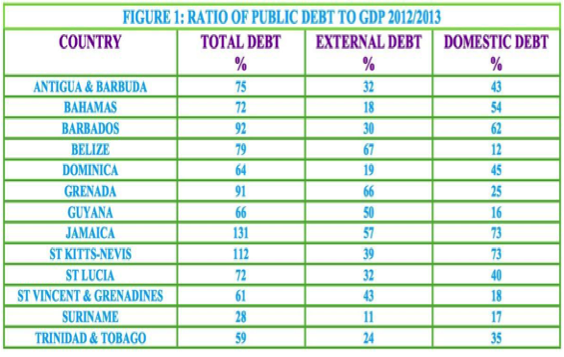

In figure 4, the Caribbean Centre for Money and Finance (CCMF) lays out the ratio of public debt to GDP of all FECC states (and the Eastern Caribbean) for the 2012/2013-time period, which highlights the growing reliance on domestic debt. According to the CCMF the prominence of domestic debt within FECC by financial institutions is due to the servicing of short term treasury bills, bonds, and other securities, along with bank loans and overdrafts.[71] The only FECC states that haven’t made the drastic switch to foreign financial institutions as their dominant creditors are the states with lower amounts of Canadian concentration—such as Belize, Guyana, St. Vincent & the Grenadines and Grenada.[72] This could be attributable to specific geographic features (Belize and Guyana both belonging to continental geographies rather than being solely island states) and the low rates of return from modern profitable FECC sectors— such as tourism—in all four of these countries, implying lower profitability rates for Canadian financial institutions.

What we also know is that in many FECC states—with the exception of Barbados—favourable policies for domestic creditors dating back to the colonial era were maintained. According to the CCMF, domestic creditors are important, because although domestic creditors receive less scrutiny that external creditors, they are still able to make “claims on the use of current fiscal revenues and therefore compete with other claims on government expenditures” in FECC.[73] This claim by the CCMF is especially troubling, considering that the private creditors of domestic debts within FECC are foreign owned, Canadian financial institutions. The CCMF contends that with this important switch to domestic debt, repayment of that domestic debt should be talked about. For instance, the repayment of domestic debts will rely on the “public’s tolerance for taxes” and “the ability of governments to meet domestic debt obligations by increasing taxes.”[74]

Although the literature on the switch to domestic debt buildup is scarce, what we do know is that domestic financing of debt is usually seen as advantageous for developing countries. This is because it increases the investor base, lowers exposure to risk if debt is denominated in the country’s currency, decreases vulnerabilities to changing capital flows, and overall tends to be safer.[75] However, these benefits all come with the assumption that there is not foreign financial concentration in the developing country. The importance of understanding the implications of high domestic indebtedness to Canadian based institutions thus becomes important because domestic debt buildup in light of concentration in foreign hands becomes negative. Thus, although the CCMF alludes to government expenditures having to take into account claims by creditors as a downside to domestic debt buildup within FECC, there is also another downside. FECC must also consider its decreasing investor base, the currency it utilizes when taking on domestic debt, the increased and continued vulnerability to changes in capital flows and the overall risk associated with weak national financial institutions. Therefore, the turn to domestic debt by FECC appears to be a result of greater (external) indebtedness.

In short, we see the continued effects of colonialism and neo-colonialism in FECC financial institutions. Canada’s financial expansion into FECC was facilitated by Great Britain’s colonial rule throughout the FECC. Canadian banks were allowed to operate based on the banks’ linkages with colonial British finance capital—providing the British with mainland financial access to North America, and maritime trade in the late 19th to early 20th century. Thus, from the historical perspective, FECC banking laws “when they were written, were written with our [Canadian] help and advice for our [Canadian] benefit.”[76] Between the 1980’s and 1990’s (as well as today), little difference in terms of bank benefits exists. Canadian banks, as in colonial times, are still able to benefit from the most profitable sectors of Caribbean economies, almost exclusively. With this sort of monopolistic and beneficial policy power, Yves Engler notes that what is unchanged from colonial times to the 1970’s is the traditionally conservative nature of Canadian banks in “releasing capital to local manufacturers, retailers and farmers.”[77] This is unsurprising in today’s context, given these banks’ subsidiary status within FECC. As subsidiary banks, Canadian banks are able to raise capital from investors and allocate small portions of their capital towards loans. Thus, due to the low amounts of loans that they are able to give to businesses, they can defend their selectivity—of only siding with profitable sectors linked to things like tourism—as part of their subsidiary status.

To Engler, Canadian lending policies have had the adverse effect of stunting the region’s development and heightening its dependency on foreign imports—as these subsidiary profits are repatriated back to Canada (see tables below).[78] Related to Engler’s findings of Canadian involvement in the financial sector, and the discriminatory policies of these banks towards small businesses and Caribbean nationals, Kevin Edmonds[79] states in his analysis of Engler’s book that “foreign multinationals can easily access credit to develop enclave industries”[80] that disproportionately benefit “industries like tourism and extractive industries such as mining [which are] being dominated by foreign interests which repatriate their profits.”[81] Of course, Canadian corporate takeover of the FECC’s financial sector is rooted in its colonial and neocolonial history, along with IMF policies which prohibited political and economic self-determination in the region.

Conclusions

This piece originally intended to discuss the limited international market access for FECC, but it turns out that the biggest obstacle to access—thus to FECC development—is the narrow ownership structure of debt and of loans from financiers, concentrated largely amongst Canadian financial institutions which give preferential treatment to dependent sectors of society that are the most vulnerable to external shocks. The financial dominance of these firms either shuts out borrowing or makes borrowing very expensive for small private firms that are not tied to profitable (super exploitative) sectors like tourism (and its associated sectors).

This piece originally intended to discuss the limited international market access for FECC, but it turns out that the biggest obstacle to access—thus to FECC development—is the narrow ownership structure of debt and of loans from financiers, concentrated largely amongst Canadian financial institutions which give preferential treatment to dependent sectors of society that are the most vulnerable to external shocks. The financial dominance of these firms either shuts out borrowing or makes borrowing very expensive for small private firms that are not tied to profitable (super exploitative) sectors like tourism (and its associated sectors).

The political economy of FECC is one structured by debt being serviced through a narrow ownership structure that contradicts FECC sovereignty—thus FECC economic security. What has been unchanged since colonialism is that the FECC, as a region, is being utilized by external entities as commodity states that enhance and enrich external interests of capital at the expense of internal solutions to development. Colonial era financial relationships—with Canadian financial firms being the main beneficiaries— have been allowed to continue due to the failure of FECC independence to effectively halt Canadian imperialism in their financial sectors. Canadian ownership did wane during turmoil beginning in the 1970’s and crises in the 1980’s, however, after the implementation of IMF SAPs by FECC states, Canadian resurgence grew. After the crisis of 2007/2008, Canadian financial institutions became the most concentrated financial institutions in the FECC region—more so than their American and European counterparts. The most adverse effect of FECC debt build-up has been the ownership of that debt which has locked the region into dependent relationships with the IMF, and increasingly to Canadian financial institutions.

By Tamanisha Jennifer John, Extramural Contributor at the Council on Hemispheric Affairs

Additional editorial support provided by Ann Jefferson, Senior Editor

Image: Cane cutters in Jamaica Taken From: Wikimedia

[1] Sumiko Ogawa, Joonkyu Park, Diva Singh, & Nita Thacker (2013). Financial Interconnectedness & Financial Sector Reforms in the Caribbean. IMF: Source: Bankscope and Fund staff calculations. Note: ECCU (June 2011); Trinidad and Tobago (March-April 2011); Jamaica (December 2010); The Bahamas (April 2011); Barbados (2010); Belize (September 2011); and Guyana (Republic Bank: 2010; and Scotia Bank: October 2011). Web: https://www.imf.org/external/pubs/ft/wp/2013/wp13175.pdf

[2] Hugues Létourneau and Pablo Heidrich (2010). Canadian Banks Abroad: Expansion and Exposure to the 2008-2009 Financial Crisis. The North-South Institute

[3] Yves Engler (2010). The Black Book of Canadian Foreign Policy. Fernwood Publishing, p.120

[4] Ibid. At the Canada-West Indies Conference of 1925, one attendee remarked: “When a country like Canada or the United States wants to build a big hotel, companies are formed and the money is supplied by either the banks or the insurance companies…in Jamaica, we can neither get the banks nor the insurance companies to [lend] us any money to put up hotels”

[5] Ibid. p.120; Peter Hudson (2010). Imperial Designs: The Royal Bank of Canada in the Caribbean. Race & Class Sage. P33-48: p.33-34: Bank Protests first starting during T&T ‘February Revolution’ which turned violent starting on April 26,1970 when protestors stormed the Royal bank of Canada’s Port of Spain headquarters. Accordingly, the Canadian bank manager shut down the branch, sent the staff home, and then went golfing. However, some also report that the manager was “startled” by the protests and what he and other Canadians saw as their new role in the Caribbean: that of the “colonialist under siege” …. “two years earlier in 1968, unemployed Black youth attacked the Royal Bank’s Kingston, Jamaica, branch and the offices of other foreign corporations and financial institutions; this was during the protests that spread from the University of the West Indies to the streets of West Kingston following the debarring of Guyanese academic and revolutionary Walter Rodney from his post at Mona and his expulsion from Jamaica.”

[6] Engler (2009). Canada in the Caribbean: A Hidden History. Rabble. Web: http://rabble.ca/news/2009/05/canada-caribbean-hidden-history; Hudson (2010). Imperial Designs. p.34: Canada has done well in projecting an image abroad as a benign, non-ideological force; liberal, tolerant, politically disinterested, high-minded in its aims, if gamely naive to its effects.

[7] Hudson (2010). Imperial Designs. p.35 C.L.R James’s talk was titled ‘On Trinidad’ and was republished in a leftist journal, Macleans, in Montreal.

[8] Ibid. p. 33-48: Hudson is mainly concerned with understanding the Royal Bank of Canada’s (RBC) imperialism in the Caribbean (English, French, and Spanish). He looks at how RBC’s imperialism has connections, both with economic and trade policy, as well as the ideologies of Canadian Anglo-Saxonism. Hudson notes that the latter also shaped the Canadian financial elite’s role in maintaining the integrity of the British and American empires. His study provides a nice background of Canada in the Caribbean, including the concentration of Canadian financial institutions within the Caribbean.

[9] Ibid. p.35

[10] Ibid. p.36

[11] Ibid. p.38

[12] Ibid. p.38

[13] Ibid. p.38-39

[14] Ibid. 39

[15] Ibid. 39: What this means is that these workers’ pay would go into these Canadian banks in their FECC country of origin, which further exploited the mobility of these workers by putting profits from banking back into Canada.

[16] Ibid. 41: One such song sings: “Everyone is bound to confess, that the Royal Bank of Canada is the very best. The reason why they have stood the test, the highest banking record to all the rest. If you think it’s not true, the ‘Guardian’ of the 31st Dec. will convince you.” Needless to say, not everyone sang these songs. Some Caribbean nationals did not sing these songs because they were seen as a threat to independence by foreign entities. Americans worried that Canadian banking power would set unfair interest rates on loans to sugar. And the British worried that songs like these would pose another threat to their empire’s legitimacy within their colonies.

[17] Ibid. p.37

[18] Ibid. p.39: “These savings accounts competed with both Indigenous credit associations and government savings banks. In some cases, such as in Haiti, the [Royal] Bank paid no interest on deposits even as it profited from lending out these previously inactive sources of Caribbean capital.”

[19] Ibid. p.41-44: Protests against Canadian banks in the region have a long history starting from the 1920’s in the Spanish and French Caribbean; and subsequently during the mid-1920’s protests against Canadian banks started in the English (FECC) Caribbean. Canadian banks were seen as a threat to British legitimacy (empire), American capital, and soon afterwards as a threat to fights for independence. In the 1970’s these protests turned violent within FECC countries that did not see themselves free of white exploitation, based on Canadian hiring practices and the granting of credit to foreign—thus white—Canadian, American, and British entities. It wasn’t until this violent pushback in the 70s that Canadians began training and hiring Caribbean-born workers, that were also recognized as white or close to white. These practices coincided with Caribbean “localization” policies, however, were never as radical as Caribbean protestors demanded.

[20] Ibid. p.43: Cuba, Dominican Republic, and Haiti present unique cases in this sense as their protests against foreign ownership of financial institutions were more radical, compared to the English-speaking Caribbean countries, during the 1920s fights for rights and ownership revolving around sugar. However, in Cuba during the Cuban revolution in the late 50’s “the Che Guevera-led Banco Nacional de Cuba seized the assets of American banks operating in the country. Canadian banks, including the Royal and the Bank of Nova Scotia were spared.” What this means is that Canadian financial ownership in Cuba, was allowed to persist despite such a radical revolution. In Haiti during the late 60’s, protests were less organized, but like those in Cuba, violent. Unfortunately, unlike Cuba, in Haiti there was a mass slaughter of Haitian communists who were the leaders of the movement to get these banks out. In the Dominican Republic, protests were hijacked by right-wing groups that also killed leftists in the country.

[21] Ibid.: p.28-29

[22] Ibid. p.44: “In 1971, the Royal Bank of Trinidad and Tobago was incorporated with 47 per cent of its shares offered to the Trinidadian public. In 1973, the Jamaican government under Manley nationalised the Royal Bank of Canada and formed the Royal Bank of Jamaica, though Montreal still controlled 48 per cent of its shares.”

[23] Ibid. p.44

[24] Ibid. p.44

[25] Ramesh Ramsaran (1992). The Challenge of Structural Adjustment in the Commonwealth Caribbean. Praeger Publishers, p.xi

[26] Stabroek News (2016). Guyana now Ranked below Haiti. Editors’ note: The Following Articles from 1989 are being reprinted as part of Stabroek News’ ongoing observances to mark its 30th Anniversary. Stabroek News. Web: www.stabroeknews.com/2016/features/30-years-of-stabroek-news/12/02/guyana-now-ranked-haiti/

[27] Ramsaran (1992). The Challenge of Structural Adjustment. p.xi; “Canadian support groups” refers to government entities that have a stake in the Canadian financial services, and also Canadian financial services themselves. “Support groups” is used because it is the more altruistic term that was first used by the IMF, even though they were anything but support groups. These were people who wanted a “stake”— in the sense that their help/recommendations would facilitate Canadian cheap buy-back for bigger, future, accumulations of capital—in Caribbean financial services for their own benefit.

[28] Ibid. p.xi-xii

[29] Jamie Swift & Brian Tomlinson (1991). Conflicts of Interest: Canada and the Third World. Chapter 2, The Debt Crisis: A Case of Global Usury (Jamie Swift & the Ecumenical Coalition for Economic Justice). Between the Lines. Kindle loc 1812

[30] Ibid. p 1-349. Kindle 1719

[31] Ibid. Kindle 1719

[32] Ibid. Kindle 1719

[33] Hudson (2010). Imperial Designs. p.44: “Canadian Bank operations in Belize were bought out by a group of investors. It sold its 48 per cent stake in Jamaica’s Royal Bank (Jamaica) to Jamaica Mutual Life Assurance as well as its stake in the Trinidad and Tobago’s Royal Bank to the Royal Bank of Trinidad and Tobago (RBTT) in 1987, an institution that had emerged as a powerful regional multinational with subsidiaries in Barbados, Jamaica, the Eastern Caribbean, Suriname, the Netherlands Antilles and Aruba.”

[34] Jamie Swift & Brian Tomlinson (1991). Conflicts of Interest, Kindle 2075: In 1987 after selling their shares in Trinidad & Tobago, along with Jamaica, A Royal Bank Executive admitted “there certainly is a need for [the IMF] to be in there as a lender and as a disciplinarian and that’s the thing all of us like about the IMF…they, perhaps like no one else, can make conditions on loans which ensure some tightening of the belt.”

[35] Hudson (2010). Imperial Designs. p.44

[36] Ramsaran (1992). Challenge of Structural Adjustment p.xi

[37] Hudson (2010). Imperial Designs. p.44

[38] Ramsaran (1992). Challenge of Structural Adjustment p.xi

[39] Hudson (2010). Imperial Designs. p.44

[40] Jamie Swift & Brian Tomlinson (1991). Conflicts of Interest. p. 1-349: Kindle 2155

[41] Emile Sanza (1978). Canadian Relations with the Caribbean and Latin America: Perspectives on Canada’s Role in the World System. McMaster University, p.23

[42] Ibid. p.35

[43] Ibid. p. 34; Ramsaran (1992). Challenge of Structural Adjustment. p.xi

[44] Jamie Swift & Brian Tomlinson (1991). Conflicts of Interest. Kindle 2289

[45] Ramsaran (1992). Challenge of Structural Adjustment. p. xi

[46] Ramesh Chaitoo (2013). Time to Rethink and Re-Energize Canada-CARICOM Relations. Caribbean Journal of International Relations & Diplomacy. vol.1, no. 1. pp. 39-67

[47] Ibid. p.41

[48] Ibid. p.41

[49] Ibid.

[50] Ibid.

[51] Paget Henry (2000). Caliban’s Reason: CH #9: Caribbean Marxism: After the Neoliberal and Linguistic Turns. Routledge, 221-246

[52] Chaitoo (2013). Time to Rethink. p. 54-55: Due to the implementation of Memorandums of Understanding MOUs towards the Caribbean region—FECC in particular—temporary visas were issued to Caribbean citizens to work in Canada as farmers. In some cases, no visa was needed at all.

[53] Ibid. p.45: According to the World Bank (WB), the seven countries with the highest emigration rates for college graduates in the world are in the Caribbean– and all belong to FECC.

[54] Ibid. p.45

[55] Ibid. p.43

[56] Ibid. p.43

[57] Ibid. p.54

[58] Ibid. p.49

[59] Ibid. p.42-43

[60] Maurice Odle (2009). The Global Financial Crisis: How Did We Get Here and How Do We Move Forward? Paper prepared for presentation at the ILO Caribbean Tripartite Conference on Promoting Human Prosperity Beyond the Global Financial Crisis, Kingston, Jamaica; Citibank from the U.S. was the only exception to this rule.

[61] Ibid., Insurance companies headquartered in Trinidad & Tobago and Jamaica that participated in the North American and European markets were exposed to risks. Additionally, real estate assets held by these countries in Florida were also significantly negatively impacted. Coupled with a decrease of main sector industries—like tourism and services—it was hard for these countries’ locally owned firms to bounce back. A Canadian corporation, in this event, was able to entirely take over FirstCaribbean International Bank, as a result of the crisis (now Canadian Imperial Bank of Commerce (CIBC) FirstCaribbean).

[62] “History of CIBC FirstCaribbean,” Web: https://www.cibcfcib.com/fcib/about-us/history.html

[63] Ibid. p.45: In 2007, Canadian banks purchased “a 50 per cent stake in the Bahamas-based Fidelity Bank & Trust International Ltd[…]In 2008, they made a bold move for the Royal Bank of Trinidad and Tobago, purchasing it for US$2.28 billion in a cash-and-stock deal for shareholders.” These purchases and acquisitions which occurred during the 2007/2008 financial crises give Canadian financial corporations the title of “the most dominant financial institutions in the Anglophone Caribbean. In the takeover of Trinidad’s RBTT, although it was promised that no job losses would occur – a promise that Trinidad’s Federation of Independent Trade Unions and Non-Governmental Organisations (FITUN) doubted in protests against the merger – RBTT Chief Executive Suresh Sookoo announced the layoffs of 500 workers a year after the deal.” Hudson concludes that there is, “a critical difference to this repetition of Canadian banks’ imperial history in the Caribbean. This time, unlike the political ferment of the 1970s, there is little awareness or concern over Canada’s ‘neo-colonialist aura’ – and this time, they are not under siege.”

[64] Christopher Thompson (2015). Bank Debt Issuance Doubles to Record Levels. Financial Times, Web: https://www.ft.com/content/e64de99a-9ffd-11e4-aa89-00144feab7de

[65] Amiri Dear (2013). Copying Canada: A Critical Analysis of the Barbados Bankruptcy and Insolvency Act. University of Toronto, p.1-70: p.7: Barbados was the only FECC state (by the time the 07/08 crises occurred) not to have such punitive laws, addressing this imbalance in 2001 through the Bankruptcy and Insolvency Act (BIA).

[66] UNDP (2015). Financing for Development Challenges in Caribbean SIDS: A Case for Review of Eligibility Criteria for Access to Concessional Financing. Web: www.undp.org/content/dam/rblac/docs/Research%20and%20Publications/Poverty%20Reduction/UNDP_RBLAC_Financing_for_Development_ReportCaribbean.pdf

[67] International Monetary Fund (2013). Caribbean Small States: Challenges of High Debt and Low Growth. IMF. Web: https://www.imf.org/external/np/pp/eng/2013/022013b.pdf

[68] Ibid.

[69] Ibid.

[70] Ibid. The chart above details all FECC states, with the only addition being Suriname (SUR) which does not belong to FECC thus its colonial financial relationships are drastically different. Acronyms within the chart are as such: Antigua & Barbuda (ATG), The Bahamas (BHS), Barbados (BRB), Belize (BLZ), Dominica (DMA), Grenada (GRD), Guyana (GUY), Jamaica (JAM), St. Kitts & Nevis (KNA), St. Vincent & The Grenadines (VCT), and Trinidad & Tobago (TTO)

[71] Caribbean Centre for Money and Finance (2014). Domestic Debt Issues in the Caribbean. CCMF. Web: www.ccmf-uwi.org/files/publications/newsletter/Vol7No10.pdf

[72] Ibid.

[73] Ibid.

[74] Ibid.

[75] Giovanna Bua, Juan Pradelli, & Andrea Presbitero (2014). Domestic Public Debt in Low-Income Countries: Trends and Structure. Review of Development Finance, vol.4, no.1. p. 1-19. Web: www.sciencedirect.com/science/article/pii/S1879933714000037

[76] Engler (2010). The Black Book of Canadian Foreign Policy. Fernwood Publishing, p.137

[77] Ibid. p.120

[78] Ibid. p.120; ECLAC (2011). Foreign Direct Investment in Latin America and the Caribbean. ECLAC: “Most of the credits granted by foreign banks are in the local currency and are channeled through their local subsidiaries.”

Web: repositorio.cepal.org/bitstream/handle/11362/1147/S1200385_en.pdf?sequence=1

[79] Kevin Edmonds (2012). Canadian Banks and Economic Control in the Caribbean. The North American Congress on Latin America (NACLA). Web: http://nacla.org/blog/2012/3/15/canadian-banks-and-economic-control-caribbean

[80] Ibid.

[81] Ibid.